When a central bank speaks with one voice, markets listen calmly. When a central bank speaks with many voices, all contradicting each other, markets get a little jumpy.

That’s exactly the situation unfolding at the European Central Bank (ECB) right now.

With the April ECB interest rate decision just days away, a parade of ECB officials has taken to podiums, press conferences, and IMF corridors to share their views, and the resulting picture is anything but unified.

For traders watching the euro, this internal debate reveals why central bank communication matters as much as the decisions themselves.

The Basics: ECB’s Current Situation

The ECB is the central bank for the 20 countries that use the euro. Its primary job is to keep eurozone inflation close to 2%. To do that, it adjusts interest rates: higher rates cool an economy and bring inflation down; lower rates stimulate growth.

Right now, the ECB is sitting at what it considers a roughly neutral rate, after completing a lengthy easing cycle through 2024–2025.

Then came the Iran war early this year. The conflict triggered a major energy shock across Europe, nearly doubling gas costs by mid-March and stoking energy-related price spikes all over.

The result: Euro Area annual inflation surged to 2.5% in March, up sharply from 1.9% in February, marking the steepest monthly increase since October 2022.

Suddenly, officials who expected to stay on hold were forced to ask: Do we need to raise rates to fight a new inflation surge? And that’s where the disagreement starts.

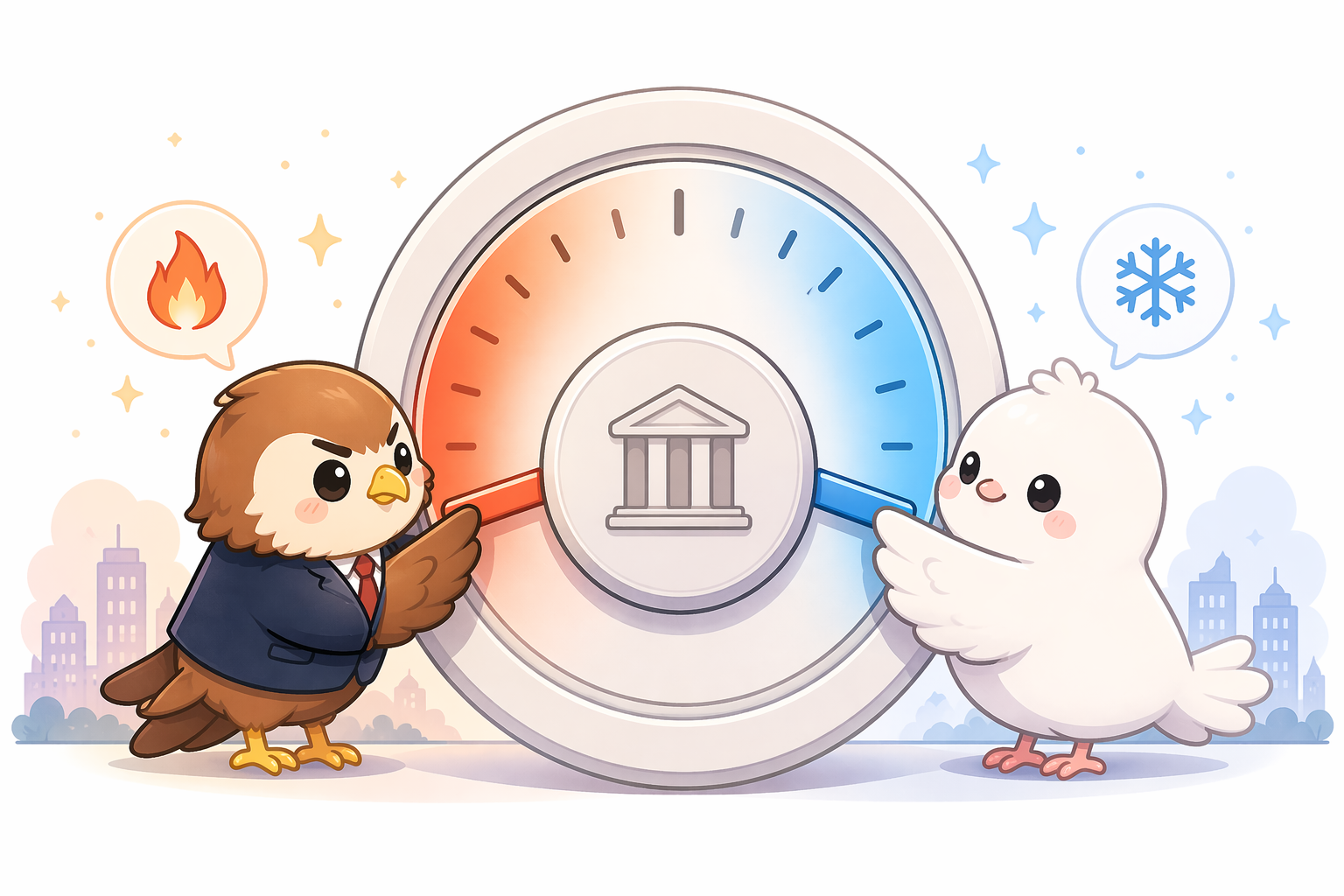

Hawks vs. Doves

Every central bank typically has two main camps of thinkers:

Every central bank typically has two main camps of thinkers:

Hawks or officials who are inclined to tighten monetary policy and prioritize fighting inflation, even if it means higher interest rates that slow economic growth.

Doves or officials who lean towards loosening monetary policy and prioritize supporting the economy, preferring lower rates even if inflation risks creep up.

Right now, the ECB’s Governing Council (its rate-setting committee) is publicly split between the two.

On the hawkish end, officials like Bundesbank President Joachim Nagel have been notably guarded. Nagel told reporters at the IMF Spring Meetings in Washington that policymakers don’t yet have sufficient information on whether a surge in energy costs will keep inflation elevated for longer — an outcome that would warrant a policy response. In other words: we’re watching, and we may have to act.

Latvia’s Martins Kazaks offered a similarly open-ended take, saying officials must monitor data as the situation unfolds and noting that markets are pricing in two rate hikes starting with June, adding: “I don’t have anything against it at the moment.”

ECB Chief Economist Philip Lane, one of the most influential voices on the Governing Council, has arguably been the most pointed on the inflation risk. In an interview with the Financial Times, Lane warned that a prolonged energy shock could cause a meaningful inflation spike, stressing: “This is not an environment where I see an argument in favor of taking a bit of risk on inflation.”

On the dovish end, there’s Lithuania’s Gediminas Simkus, whose comments this week offered perhaps the clearest near-term signal from the cautious camp. Simkus said the ECB should not raise interest rates in April, citing the deposit facility rate as broadly appropriate given that core inflation has remained near the 2% target despite the headline spike.

Meanwhile, behind closed doors, the picture appears even more nuanced. According to reporting from Econostream Media, which spoke with eight ECB officials on background at the Washington IMF meetings, one official said June would bring “more information, not an obligation,” another said flatly that “June is not a given,” and a third stressed there was “no automaticity” from an April hold to a June move.

The core debate is that if the shock proves temporary, the ECB can look through it; if it persists, it cannot ignore it.

In other words, everything hinges on whether the energy price spike caused by the war will fade or bleed into wages, service costs, and broader price expectations — a process economists call second-round effects.

Promoted: Trading a divided ECB takes more than gut feel. It demands structure, discipline, and access to real capital.

Lux Trading Firm gives serious traders up to $10M in funding, with evaluation fees refunded after Stage 1 and pathways to long term payouts.

Learn More at Lux Trading Firm

Disclosure: To help support our free daily content, we may earn a commission from our partners if you sign up through our links, at no extra cost to you.

What Does This Mean for EUR?

This disagreement among ECB officials is creating a particularly tricky environment for EUR/USD traders.

On one hand, any signal that the ECB is leaning toward rate hikes would typically be euro-positive. Higher rates make euro-denominated assets more attractive to global investors, increasing demand for euros and potentially pushing EUR/USD higher. Earlier this month, markets were pricing in up to three ECB rate hikes following the dramatic shift in expectations amid the Middle East conflict.

On the other hand, a deeply divided ECB may struggle to deliver a clear signal either way, and markets dislike ambiguity. Financial markets are currently pricing in a hold at the April 29–30 meeting, followed by a potential hike in June, with the majority expecting the ECB’s key rate to reach at least 2.5% by year-end.

The range of voices — Lane warning firmly against complacency on inflation, Simkus urging patience in April, Kazaks keeping June on the table, and Nagel calling everything “very cloudy” — means each upcoming data print and each new official comment carries the potential to meaningfully shift EUR/USD in either direction.

Looking ahead, the euro may stay highly sensitive to every ECB official comment between now and June, as the market rapidly re-prices rate expectations based on whether the next speaker sounds more hawkish or more dovish.

The Bottom Line

Hawks vs. doves matters for the euro. When ECB officials signal rate hikes (hawkish), EUR/USD tends to be supported. When they signal caution (dovish), the euro may face pressure. Right now, both camps are speaking all at once.

The Iran war changed the trajectory. An energy shock flipped the ECB’s near-term inflation outlook, turning a straightforward hold-and-watch situation into a live debate about whether rate hikes are needed for the first time since 2023.

“Data dependent” is not a cop-out. Each incoming eurozone inflation print, wage figure, and energy price move will likely shift this debate and with it, the euro.

What to Watch Next

Beyond this week’s flash eurozone PMI releases, the ECB’s April 29–30 meeting is the next major focus: a hold is widely expected, but the statement’s language and President Christine Lagarde’s press conference will be closely parsed for June signals.

After that, watch eurozone CPI data for April (released late April/early May), Q1 wage growth figures, and any further commentary from Lane on second-round effects. The June 11 ECB meeting is increasingly shaping up as the one that truly matters.

BabyPips Premium Annual Members have exclusive access to our highest-tier partnership deal: 30% off your first purchase of a TradeZella annual subscription! To level up the rate of progress towards mastering your performance and psychology, TradeZella’s AI-powered journaling and backtesting tools are the industry gold standard.

This discount effectively covers a large portion of an annual BabyPips Premium subscription!To Claim the Exclusive 30% off, email us at [email protected] to verify membership status and receive the promo code. Please reference “TradeZella Annual Plan Promo Code” in your email subject line.